Increasing US manufacturing will require increasing manufacturing productivity. We explore the existing technologies that can be transformative for US productivity, and what it will take for them to be applied at scale.

In Part 1 of this two-part series co-authored with Eclipse, we shared that the US is uncompetitive in many different types of manufacturing because of structurally higher costs, most notably labor, and because decades of offshoring have weakened the US industrial base, leaving limited capacity to support a self-reinforcing build-out of the manufacturing sector. Tariffs are unlikely to meaningfully close this cost differential or create manufacturing capacity for goods the US barely produces at all, such as apparel or consumer electronics.

At the same time, the US has a lot going for it: an incredibly large domestic consumer market, low energy costs, flexible labor markets, and a government that has clearly signaled its support for the manufacturing sector. Capitalizing on these advantages and overcoming the structural headwinds to US manufacturing to make it more competitive will likely require making manufacturing more productive, so that higher output justifies the higher production costs in the US.

There are new technologies that have the power to be transformative and currently exist, but scaling them up will likely take the better part of a decade. Targeted tariffs can work to lower the hurdle these new technologies have to clear in terms of reducing production costs and improving efficiency before it is profitable to invest in them and build out domestic manufacturing capacity.

A copy/paste of the prevailing manufacturing processes from other countries will not satisfy the reindustrialization appetite of US policy makers, as it would be too costly, slow, and reliant upon the insufficient US labor pool of skilled and interested manufacturing technicians and trade workers. To increase US onshore manufacturing productivity to a level where volumes could satisfy domestic demand, with a manufacturing capacity footprint limited by construction and installation timelines and low worker interest and qualifications, the US must leverage advanced technologies to increase productivity by one to two orders of magnitude.

Technologies that are both a) scale-ready and b) capable of moving the needle for US manufacturing productivity include automation, computer vision, additive manufacturing, and machine condition monitoring. Technologies that are in earlier phases of development but potentially even more transformative include generative AI (simulation and digital twinning) and embodied AI.

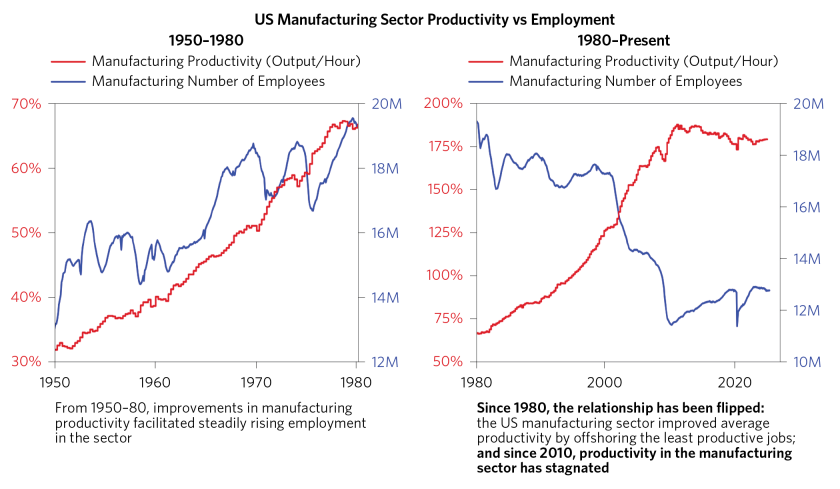

A cursory glance suggests productivity in the manufacturing sector has stagnated since 2010, but a deeper look highlights a secular turning point of stagnation right around 1980. In the decades leading up to 1980, steadily rising productivity growth in the manufacturing sector supported economic growth, more production, and, ultimately, more employment in the sector. But since 1980, the relationship between productivity growth and employment in manufacturing has been flipped, and manufacturing only got more productive as employment fell. This is because the US offshored the least productive manufacturing sectors (like apparel manufacturing), raising the average level of manufacturing productivity through process of elimination.

In the rest of this report, we share more detail on each of the technologies that could work to improve US manufacturing productivity and describe how the process of adopting these technologies will take time.

The Technologies That Could Make American Manufacturing More Productive

1. Software-defined manufacturing and automation

More than 80% of US warehouses today have no automation, with only 141 robots per 10,000 manufacturing employees. Automation can take many shapes and forms, and in manufacturing settings, humanoid robots are currently less efficient and effective than other automation solutions. At Tesla’s manufacturing sites, for example, billions invested in robotic cells and manufacturing automation have streamlined production and increased gross margin.

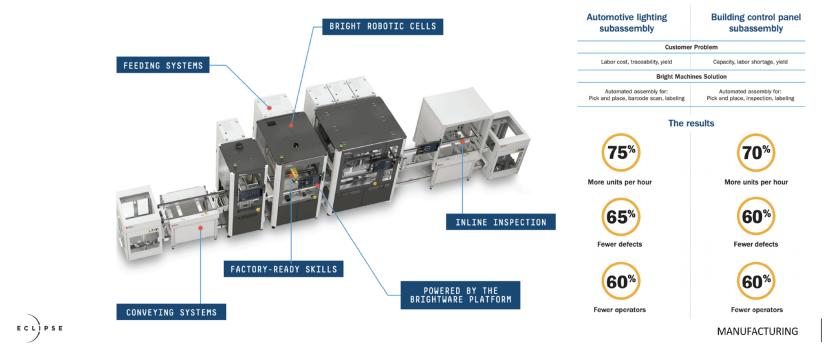

For smaller electronics with advanced components like GPUs that are changing quarter over quarter, microfactories with programmable inputs are ideal for high-mix, low-volume assemblies. Increasing numbers of manufacturing automation players in the market are leveraging software and low-cost robotics to automate full lines for end-device and goods assembly, not just parts or subassemblies. For example, the below series of robotic cells can take a low-code/no-code set of commands paired with design files and produce many different types of quality-assured systems as outputs, from data center servers to hand drills, at increased throughput (75%) and fewer defects (-65%) than typical assembly processes.

The US lags in industrial automation relative to the rest of the world, with low levels of industrial robot adoption in US factories compared to other developed economies. Government policy can play a role here. For example, Korea’s government-led robotics industrial policy includes an investment commitment of $2.26 billion by 2030, streamlining of regulatory hurdles, and investing in skilled robotics training courses for 15,000 workers.

2. Computer vision

Advances in AI and computer vision, including vision transformers (ViT), which can detect objects 30% faster than convoluted neural networks (CNNs), and other forms of edge AI like Nvidia’s Jetson processors, mean existing camera infrastructure can play a major role in nonintrusive operational productivity in industrial environments. Computer vision efficiency has the capacity to radically improve operational efficiency across multiple types of industrial environments, from retail, where real-time stock tracking via computer vision and RFID can reduce out-of-stock events by 40%, to certain types of manufacturing defect detection and lowering the frequency of industrial safety incidents.

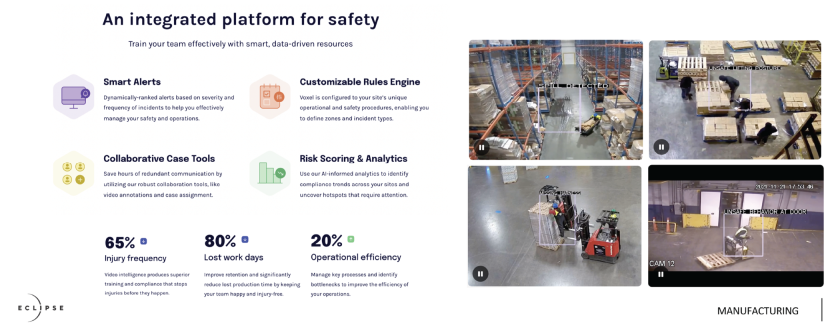

Below, we show an example of computer vision being used to improve safety in an industrial environment. The presence of such systems (with a managerial feedback loop to operators on the ground) has proven to reduce incidents by 60-80% and increase operational efficiencies by around 20%.

3. Additive manufacturing

Additive manufacturing (also known as 3D printing) has evolved significantly, and major brands are beginning to adopt leading-edge solutions. Some solutions are 20x faster and a fraction of the carbon footprint of traditional fabrication techniques. Certain advanced additive technologies can rapidly produce even complex, durable designs such as fuel nozzles for jet engines or spinal implants. Advances in additive manufacturing are key to any near-shored supply chain strategy.

Below, we show key statistics reported by one industrial-scale 3D metal additive manufacturer based outside of Boston:

4. Machine condition monitoring

Mechanical issues account for 10-15% of losses in manufacturing productivity. Unplanned downtime is a significant loss-making scenario in manufacturing, and scheduled maintenance has historically been an inefficient but necessary evil. Today’s machine-monitoring solutions offer not only constant monitoring and alerting across most equipment types, but also predictive maintenance capabilities and machine learning based on large datasets across many customers and machine types, and are capable of reducing unplanned downtime by more than 50%.

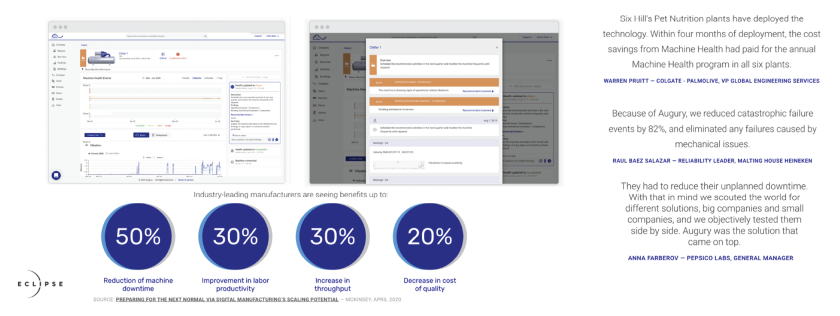

Below, we show UI and results by machine condition monitoring company Augury:

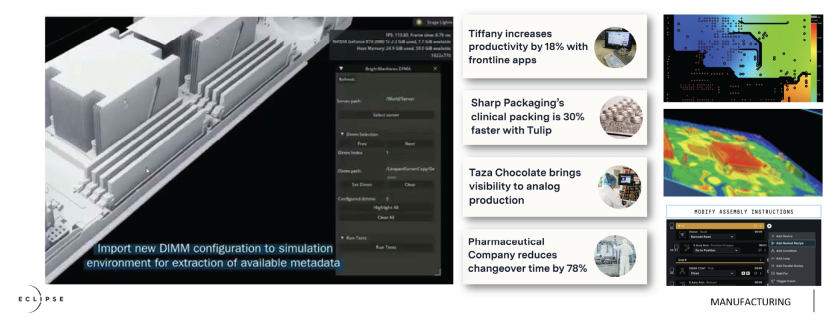

5. Generative AI and low-code/no-code modern design tools

Traditional manufacturing execution systems (MES) were built for stability and meant to last but have struggled to keep up with the fast-paced, complex market demands and disruptions of today. An increasing number of technologies have targeted manufacturing design simulation and MES integrations that enable technicians to make modifications without complex programming or expensive change orders. Generative AI is increasingly usable in the design and simulation of new systems (mechanical, electrical, thermal, and full system integration), enabling a radical reduction in cost and speed to market, as we show below.

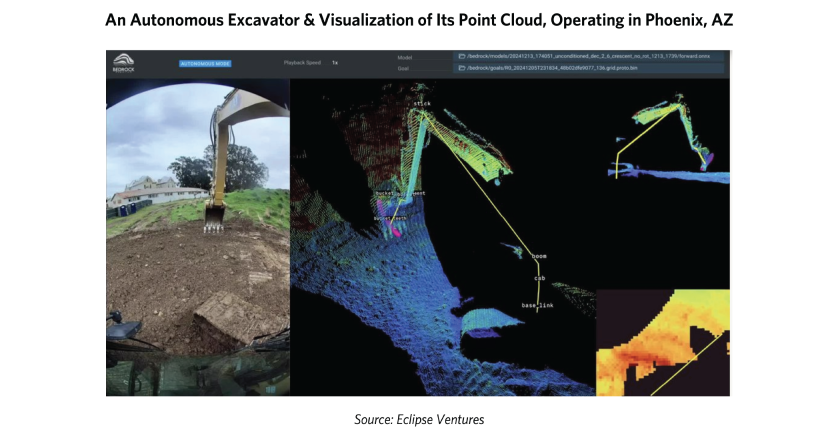

6. Embodied AI and robotics

As evidenced by Waymo’s self-driving cars expanding across geographies, today’s robotics tech stack has advanced far beyond what seemed possible even just a few years ago. Self-supervised learning (SSL) models and large models (language and video) are revolutionizing robotics. Each AI era—ImageNet for vision and transformers for language—is defined by its toughest data challenges. The next frontier—embodied AI—is a term for advanced, applied robotics, like Waymo vehicles, and is already taking hold across industrial and manufacturing environments. The lessons from the first million autonomous miles driven at Waymo can now be applied to adjacent industries (such as construction and other heavy equipment operations, as pictured below).

Adding industrial capacity (building plants, fabricating tooling, producing steel, and other key inputs) is as important as improving manufacturing throughput, and embodied AI’s capabilities to support large-scale, foundational industrial workloads in construction, warehousing, agriculture, and manufacturing may be critical to the generational transformation needed for a broader-scale US manufacturing capacity build-out.

The Process of Adopting These Technologies Will Take Time, Making the Revival of US Manufacturing a Process That Will Likely Take a Decade, If Not Longer

The United States is a decade away from the scale and scope of “lights-out” manufacturing that could enable it to rival the rest of the world’s manufacturing output to satisfy the US’s own end-to-end demand, at a similar or lesser cost.

While the current scale and impact of advanced technologies in American industrial production is low outside of low-volume defense manufacturing, several key technological advances are having a positive impact on US industrial productivity. Unfortunately, 98% of manufacturers in the United States are small-to-medium enterprises and are relatively underpenetrated by technologies capable of driving significant growth in manufacturing productivity.

Essentially, the low levels of deployment of these increasingly mature technologies in the US today are limited not by technical readiness or maturity, but by commercial adoption and willingness to invest in advanced capabilities and improved manufacturing throughput.

This research paper is prepared by and is the property of Bridgewater Associates, LP and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, Bridgewater's actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing and transactions costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. Any such offering will be made pursuant to a definitive offering memorandum. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. No discussion with respect to specific companies should be considered a recommendation to purchase or sell any particular investment. The companies discussed should not be taken to represent holdings in any Bridgewater strategy. It should not be assumed that any of the companies discussed were or will be profitable, or that recommendations made in the future will be profitable.

The information provided herein is not intended to provide a sufficient basis on which to make an investment decision and investment decisions should not be based on simulated, hypothetical, or illustrative information that have inherent limitations. Unlike an actual performance record simulated or hypothetical results do not represent actual trading or the actual costs of management and may have under or overcompensated for the impact of certain market risk factors. Bridgewater makes no representation that any account will or is likely to achieve returns similar to those shown. The price and value of the investments referred to in this research and the income therefrom may fluctuate. Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur. Investments in hedge funds are complex, speculative and carry a high degree of risk, including the risk of a complete loss of an investor’s entire investment. Past performance is not a guide to future performance, future returns are not guaranteed, and a complete loss of original capital may occur. Certain transactions, including those involving leverage, futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Fluctuations in exchange rates could have material adverse effects on the value or price of, or income derived from, certain investments.

Bridgewater research utilizes data and information from public, private, and internal sources, including data from actual Bridgewater trades. Sources include BCA, Bloomberg Finance L.P., Bond Radar, Candeal, CEIC Data Company Ltd., Ceras Analytics, China Bull Research, Clarus Financial Technology, CLS Processing Solutions, Conference Board of Canada, Consensus Economics Inc., DTCC Data Repository, Ecoanalitica, Empirical Research Partners, Energy Aspects Corp, Entis (Axioma Qontigo Simcorp), Enverus, EPFR Global, Eurasia Group, Evercore ISI, FactSet Research Systems, Fastmarkets Global Limited, The Financial Times Limited, Finaeon, Inc., FINRA, GaveKal Research Ltd., GlobalSource Partners, Harvard Business Review, Haver Analytics, Inc., Institutional Shareholder Services (ISS), The Investment Funds Institute of Canada, ICE Derived Data (UK), Investment Company Institute, International Institute of Finance, JP Morgan, JTSA Advisors, LSEG Data and Analytics, MarketAxess, Metals Focus Ltd, MSCI, Inc., National Bureau of Economic Research, Neudata, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Pitchbook, Political Alpha, Renaissance Capital Research, Rhodium Group, RP Data, Rubinson Research, Rystad Energy, S&P Global Market Intelligence, Sentix GmbH, SGH Macro, Shanghai Metals Market, Smart Insider Ltd., Sustainalytics, Swaps Monitor, Tradeweb, United Nations, US Department of Commerce, Visible Alpha, Wells Bay, Wind Financial Information LLC, With Intelligence, Wood Mackenzie Limited, World Bureau of Metal Statistics, World Economic Forum, and YieldBook. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy. Data leveraged from third-party providers, related to financial and non-financial characteristics, may not be accurate or complete. The data and factors that Bridgewater considers within its research process may change over time.

This information is not directed at or intended for distribution to or use by any person or entity located in any jurisdiction where such distribution, publication, availability, or use would be contrary to applicable law or regulation, or which would subject Bridgewater to any registration or licensing requirements within such jurisdiction. No part of this material may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without the prior written consent of Bridgewater® Associates, LP.

The views expressed herein are solely those of Bridgewater as of the date of this report and are subject to change without notice. Bridgewater may have a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Those responsible for preparing this report receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.