Without more domestic manufacturing, tariffs are likely to result in lower margins and higher prices. In Part 1 of this series, we explore the structural pressures that make growing US manufacturing so challenging.

This report is a collaboration between Bridgewater Associates and Eclipse, a leading industrial technology investment firm, focused on companies that transform physical industries critical to people’s lives. This research draws on a series of conversations with manufacturing professionals in Eclipse’s network, Eclipse’s expertise in industrial technology, and Bridgewater’s macroeconomic expertise. Aidan Madigan-Curtis, who co-authored this BDO, is a general partner at Eclipse and a Bridgewater alumnus. Aidan invests across core, disruptive themes in today’s world, including geopolitical decoupling, supply chain dislocation, energy transition, manufacturing onshoring, and industrial autonomy. She also sits on 10 corporate boards spanning defense and industrial sectors and a broad array of technologies, including the Internet of Things, computer vision and AI, autonomy, and robotics.

With the US’s embrace of modern mercantilism, policy makers are increasingly trying to leverage economic policy to enhance national security and strength, as opposed to a laissez-faire approach of allowing free markets to drive economic growth. As such, revitalizing the domestic manufacturing base is a core priority of the Trump administration, given the importance of supply chain security, a robust defense industrial base, and the potential benefits to key constituencies like manufacturing workers.

Bringing back US manufacturing will be a Herculean task—the US economic system has been optimized to employ people in the highest-value-added industries, and much of what can be done more efficiently elsewhere has been outsourced. Reordering the entire system to produce more manufacturing will require significant shifts in labor and capital, and the accumulation of new knowledge and expertise.

The administration has enacted sweeping tariffs in pursuit of reviving domestic manufacturing. Whether these policies succeed in increasing US manufacturing or simply result in higher costs that companies either absorb in margins or pass on to consumers will depend on: 1) existing US manufacturing capacity for the goods being tariffed, 2) how much tariffs close the cost differential between producing abroad and producing in the US, and 3) how difficult and time-consuming it is to scale up new industrial capacity. In this report, we share our thinking on the possibility of reshoring manufacturing to the US and how much of a difference tariffs can make. Our key takeaways:

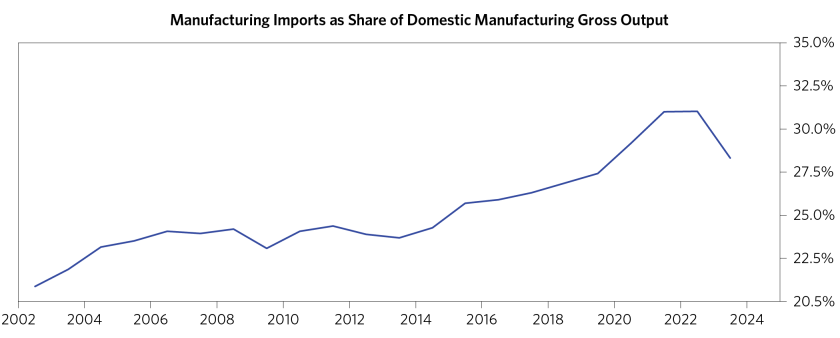

- The US starts from a place of limited but not nonexistent manufacturing capacity. Right now, the US imports roughly 40% of the goods it consumes, both directly and indirectly through domestic manufacturers’ use of imported inputs, as it has become increasingly dependent on imports over the past several decades. Certain goods consumption in the US, like apparel, is almost entirely imported, as labor is a large share of the total cost, and these goods can be produced much more cheaply outside the US. Tariffs on these kinds of goods are especially likely to be passed on to the consumer, given the lack of any viable competition from domestic producers any time soon.

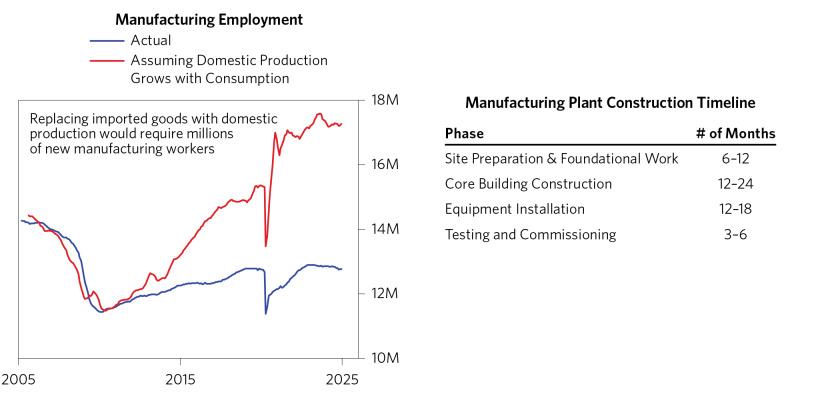

- The lack of sufficient scaled manufacturing capacity across tooling, electronics, semiconductor supply chains, and critical equipment inputs is a major barrier to scaling up manufacturing capacity in the near term. Even for goods where the US does have some domestic manufacturing capacity (e.g., in autos, agricultural and defense equipment, and pharmaceutical manufacturing), there are major hurdles to scaling up production significantly in the near term, given the time it takes to build manufacturing capacity and the shortage of manufacturing labor, particularly workers with specialized skills. A rough estimate is thatnearly 5 million additional workers would have been needed for manufacturing jobs to supply the increase in US goods consumption that occurred over the past 20 years. As such, even for goods the US has some ability to produce domestically, tariffs may not do much in the short term to increase domestic production market share, though they can potentially help in the long term.

- The US faces significant challenges in terms of cost competitiveness. Globalization drove the offshoring of US manufacturing toward economies with much cheaper production costs. In some cases, the cost differential is large enough that even 25% tariffs don’t close the gap—for example in India, where productivity-adjusted wages are 30% lower compared to the US. The dollar’s secular strength has also effectively raised the cost of goods produced in the US relative to foreign-produced goods and acted as a headwind to US manufacturing competitiveness.

- Broad tariffs can be counterproductive in some cases, where the necessary inputs to build manufacturing capacity—the “machines that build the machines,” as one of our interview subjects put it—are imported, and tariffs make it even costlier to manufacture domestically. Many of these inputs are only produced by a few companies in a small number of countries, with market share dominated by Europe and by China.

- One of the most durable ways to increase the viability of manufacturing in the US is to increase the productivity of the manufacturing sector (which is likely to be only marginally impacted by tariffs) and thereby decrease the relative importance of higher labor costs. Productivity in the US manufacturing sector has been stagnant for the past 15 years, but there are new technologies that have the power to be transformative. We discuss these technologies in greater detail in Part 2 of this report.

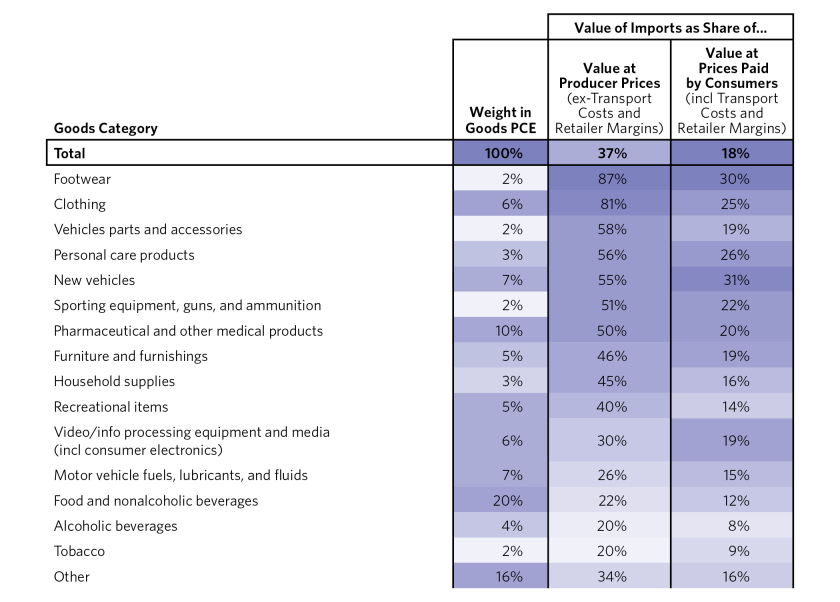

The table below breaks down US consumer spending by type of good, and the share of that consumption from imports (either directly, or through domestically produced goods with imported inputs). We show imports as a share of producer value of all US goods consumption, i.e., excluding any value add that the Bureau of Economic Analysis attributes to transportation costs or retailer margins—for that figure, the US import share is 37%. Relatively low-value goods, like footwear and clothing, are heavily imported (80-90%). Food is the main sizable consumption item that the US mostly produces at home. Many goods, such as new motor vehicles, household appliances, and pharmaceuticals, are significantly but not entirely imported (~50-60%) and have domestic manufacturing capability that could be scaled up.

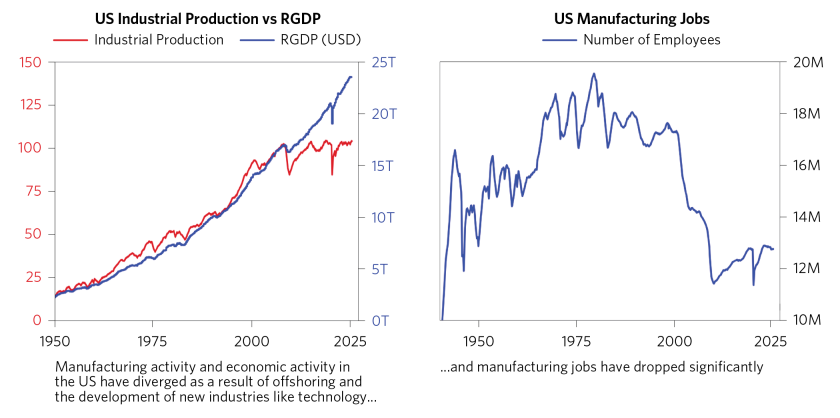

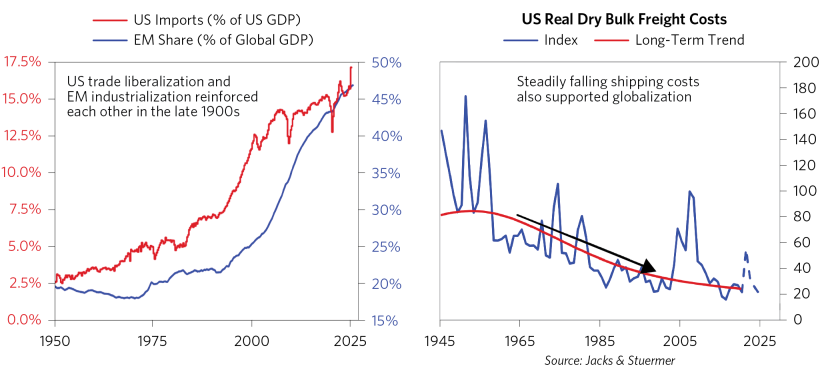

Offshoring of manufacturing in the US has been a multidecade process, driven by a combination of falling shipping costs, rising labor cost differentials between the US and foreign economies, and industrialization in emerging market economies. This process slowly began in the post-war era but accelerated in the 1990s and early 2000s, particularly with the inclusion of China into the WTO. As such, the number of manufacturing jobs in the US has fallen precipitously, but the importance of manufacturing to US economic growth has also declined, as the US economy continued to develop a comparative advantage in sectors like high-value services and technology.

Below, we walk through the near-term and structural challenges to bringing back US manufacturing and the potential path forward.

Near-Term Challenges to Bringing Back Manufacturing

The biggest near-term challenge to bringing back manufacturing to the US—and the reason why tariffs are more likely to result in a combination of higher prices and lower margins than in increased domestic producer market share—is that the US simply does not have the labor and industrial capacity to produce many goods domestically and faces constraints on the ability to scale up production in the near term.

This is especially true of goods that the US doesn’t produce much of, such as apparel. For goods the US does produce, the picture is more mixed. The biggest near-term challenge would be scaling up production to meet US demand—the US manufacturing workforce has shrunk significantly over the past several decades, as employment has instead shifted more toward the services sector.

As one rough way of penciling out what would be required—nearly 5 million additional workers would be needed for manufacturing jobs if the US manufacturing workforce had grown at the same rate US goods consumption grew over the past 20 years. Finding those workers would likely prove very challenging, as many require specialized skills, and according to the National Association of Manufacturers’ Outlook Survey, nearly 50% of manufacturing firms list “Attracting and Retaining a Quality Workforce” as a primary business challenge.

In addition to the labor-related challenges with scaling up manufacturing capacity, constructing new heavy industrial manufacturing facilities can take anywhere between three to five years, and sometimes even longer for highly complex processes, such as semiconductor fabrication or pharmaceutical manufacturing.

Bringing the manufacturing capacity onshore or even nearshore to support the trillions of dollars of goods purchased by United States consumers and businesses annually would likely require more than a trillion dollars of investment across the manufacturing supply chain (for reference, total annual business fixed investment in the US is about $4 trillion). Hundreds of manufacturing sites would need to break ground, and hundreds of billions of dollars in heavy equipment would need to be procured across systems from chemical fabrication equipment (vats, reactors, boilers) to pick-and-place systems, lasers, molders, drills, conveyors, ovens, and advanced robotic systems.

Almost all manufacturing capacity to support the global electronics market—including layers of upstream supply chains for integrated circuit fabrication, consumable materials chemical synthesis, specialty sensors (like MEMS and haptics), flexible printed circuit boards, OLED displays, glass and metal enclosures, and GPUs to support the global electronics market—does not exist onshore in the US.

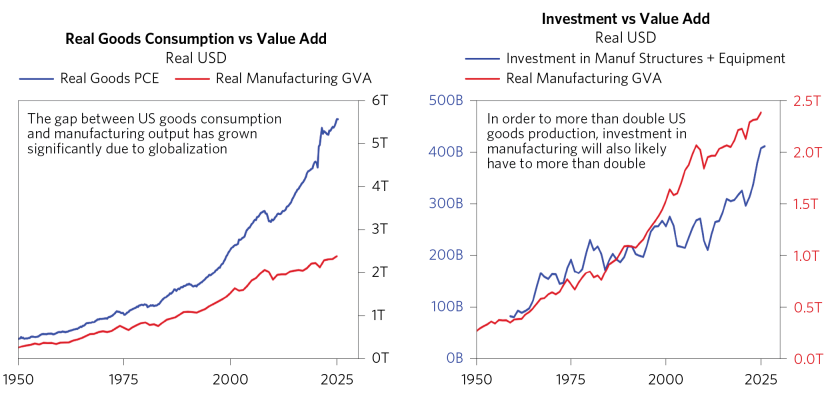

As one rough proxy, there is currently a ~$3 trillion dollar gap between US manufacturing output and US goods consumption, as shown in the left chart below, and US manufacturing output has roughly linearly scaled with investment in US manufacturing, as shown in the right chart. So it is entirely plausible that to more than double current US manufacturing output to match goods consumption, annual investment will have to double from just under half a trillion dollars to over a trillion (and possibly more, given the lack of an existing industrial base to compound off of in certain sectors).

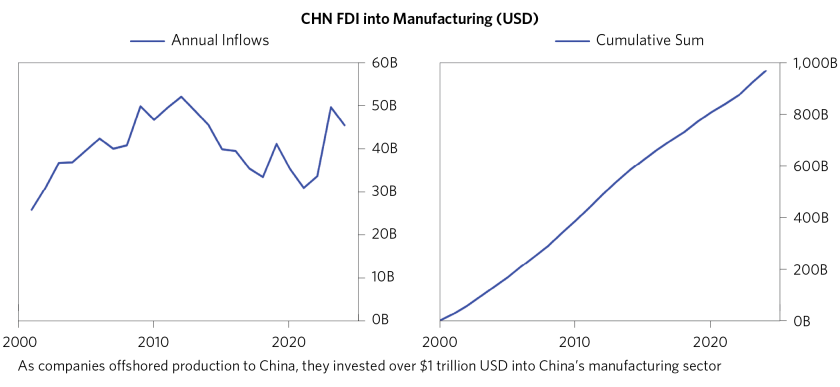

As another perspective, over the past 20 years, foreign companies have invested roughly a trillion dollars into China’s manufacturing sector.

The challenges of scaling up production were a key theme in the conversations Bridgewater and Eclipse had with industry leaders. We summarize some of those discussions below:

- A former automotive executive noted that when building a factory in Illinois, the number one constraint he faced was finding and hiring skilled labor, and that in many cases, he had to hire (hundreds of) these workers from abroad. These roles included welders, robot programmers, electricians, and skilled technicians.

- One Intel executive noted that significant delays in their semiconductor fabrication plant construction over the past several years in Arizona were due not to their 3,000 worker shortage in semiconductor technicians (which is also an issue) but initially to the 8,000 trade-worker shortage they faced hiring electricians, construction workers, industrial plumbers, and HVAC technicians to build the fabs in the first place.

- When it comes to manufacturing the types of electronics that power all devices—from phones and computers to cars, airplanes, and medical devices—the vast majority of this global manufacturing capacity exists in Asia.

- One CEO providing excavation and other earthmoving construction work for a large, 600,000 cubic-yard Midwestern paper mill noted that just the earthmoving (excavation, leveling, and other basics) would likely take 12 months or more, with more than 6 months of continuous excavation work.

- More broadly, there is a vast mismatch between millions of unfilled industrial job postings and a US population that is neither qualified nor experienced in picking up more welding torches and hand drills. The gap between supply and demand of skilled industrial labor only widens every day as skilled Baby Boomers opt for retirement, and millennials and Gen Zers have a demonstrated attraction to digital-native versus physical labor.

Structural Challenges to Bringing Back Manufacturing

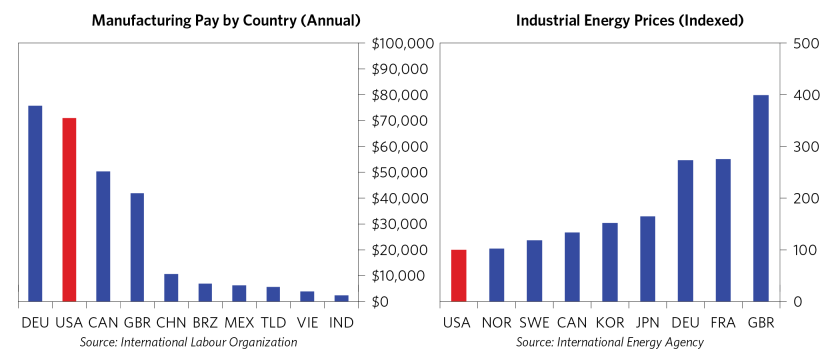

The US’s biggest comparative disadvantage is its cost of production. Globalization facilitated the offshoring of manufacturing in the US toward economies with much cheaper costs of production, particularly for goods with relatively low manufacturing value add that are also easy to ship internationally. Higher labor costs in the US are the predominant driver of this cost differential, though higher real estate costs also play a role. Energy prices, meanwhile, are a modest support.

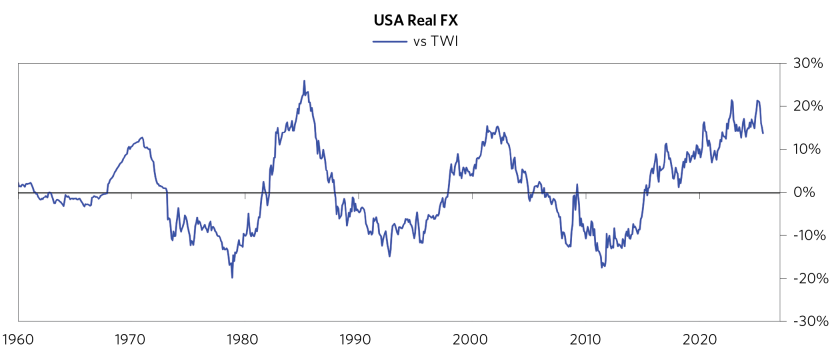

A secularly strong dollar has also effectively raised the cost of US-produced goods relative to foreign-produced goods and contributed to the decline of US manufacturing competitiveness.

Numerous conversations with industry leaders shed further light on the cost disadvantages of producing in the US compared to abroad:

- When a publicly traded manufacturer of industrial sensors and connected devices searched for an onshore option to mass-produce their systems and sensors, the result was that there were merely a handful of electronics manufacturers that could support a forecast with more than prototype-scale and the relative manufacturing value added was anywhere from 5-20x more per part. Furthermore, it was nonsensical for this company to manufacture onshore in the US when the rest of the component and assembly supply chain, plus manufacturing know-how (previously built, similar designs by a knowledgeable workforce), existed predominantly overseas.

- As an indication of the disadvantages of the US, many brands that are moving to a “China+1” (or +2 or +3) strategy are not moving to the US but rather to other economies in Asia. One logistics leader responsible for importing and brokerage for the largest retailers and electronics companies in the US claimed that “China is losing share as a country of origin rapidly” and pointed to “Thailand, Malaysia, Vietnam, [and] Cambodia growing between 40-140% Y/Y as the stated country of origin”—and that “this trend has accelerated in the last six months.”

Tariffs Can Be Counterproductive to Rebuilding US Manufacturing, Given Critical Industrial Inputs That Are Hard to Replicate and Only a Few Countries Are Able to Produce

Tariffs risk exacerbating the US’s cost-competitiveness challenges by raising the cost of many input goods that domestic manufacturers import. Over the past several decades, supply chains have increasingly globalized, and the share of imported content in domestic manufacturing output has steadily risen. Europe and China in particular dominate global market share for many industrial goods needed to set up domestic manufacturing capacity in the first place, such as machinery and electrical equipment. Many of these machines, such as semiconductor lithography machines or certain kinds of advanced robotics, are highly specialized and only produced by a few companies (or as little as one company) in a small number of countries.

This was also a frequent theme in our conversations:

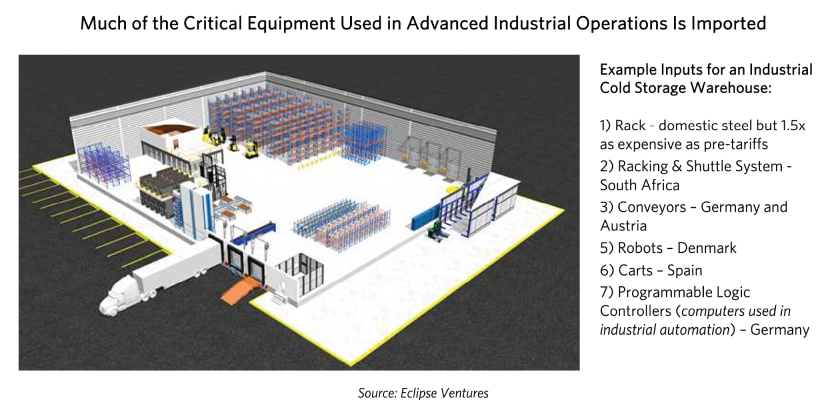

- As American companies attempt to increase deployments of robotics and other automation tools onshore, they face significant limitations, as the high-quality racking, robotic arms, hydraulic systems, PLCs, and hundreds of millions of other specialty parts for advanced manufacturing capabilities originate in Europe (Germany, Denmark, Spain), Asia (South Korea, Japan, China, Taiwan), Canada, Mexico, and even South Africa. Essentially, as one former Tesla and Rivian manufacturing executive relayed, America is dependent on imports to “build the machines that build the machines.”

- One of the US’s largest cold chain businesses is a large builder of American onshore industrial capacity. Their leadership described the challenges of building warehousing capacity—from the uncertainty of costs from the time key components left the ports in Europe and Asia, to the moment they arrived on US soil. These new warehouses require a significant amount of steel (which now faces a 50% tariff), and this warehousing player’s infrastructure relies on critical imports because foreign companies and their products are the only qualified manufacturers in the world of these specialty parts.

In Part 2 of this report, we’ll walk through what, given these challenges, could change in order to make US manufacturing more feasible.

This research paper is prepared by and is the property of Bridgewater Associates, LP and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, Bridgewater's actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing and transactions costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. Any such offering will be made pursuant to a definitive offering memorandum. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. No discussion with respect to specific companies should be considered a recommendation to purchase or sell any particular investment. The companies discussed should not be taken to represent holdings in any Bridgewater strategy. It should not be assumed that any of the companies discussed were or will be profitable, or that recommendations made in the future will be profitable.

The information provided herein is not intended to provide a sufficient basis on which to make an investment decision and investment decisions should not be based on simulated, hypothetical, or illustrative information that have inherent limitations. Unlike an actual performance record simulated or hypothetical results do not represent actual trading or the actual costs of management and may have under or overcompensated for the impact of certain market risk factors. Bridgewater makes no representation that any account will or is likely to achieve returns similar to those shown. The price and value of the investments referred to in this research and the income therefrom may fluctuate. Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur. Investments in hedge funds are complex, speculative and carry a high degree of risk, including the risk of a complete loss of an investor’s entire investment. Past performance is not a guide to future performance, future returns are not guaranteed, and a complete loss of original capital may occur. Certain transactions, including those involving leverage, futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Fluctuations in exchange rates could have material adverse effects on the value or price of, or income derived from, certain investments.

Bridgewater research utilizes data and information from public, private, and internal sources, including data from actual Bridgewater trades. Sources include BCA, Bloomberg Finance L.P., Bond Radar, Candeal, CEIC Data Company Ltd., Ceras Analytics, China Bull Research, Clarus Financial Technology, CLS Processing Solutions, Conference Board of Canada, Consensus Economics Inc., DTCC Data Repository, Ecoanalitica, Empirical Research Partners, Energy Aspects Corp, Entis (Axioma Qontigo Simcorp), Enverus, EPFR Global, Eurasia Group, Evercore ISI, FactSet Research Systems, Fastmarkets Global Limited, The Financial Times Limited, Finaeon, Inc., FINRA, GaveKal Research Ltd., GlobalSource Partners, Harvard Business Review, Haver Analytics, Inc., Institutional Shareholder Services (ISS), The Investment Funds Institute of Canada, ICE Derived Data (UK), Investment Company Institute, International Institute of Finance, JP Morgan, JTSA Advisors, LSEG Data and Analytics, MarketAxess, Metals Focus Ltd, MSCI, Inc., National Bureau of Economic Research, Neudata, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Pitchbook, Political Alpha, Renaissance Capital Research, Rhodium Group, RP Data, Rubinson Research, Rystad Energy, S&P Global Market Intelligence, Sentix GmbH, SGH Macro, Shanghai Metals Market, Smart Insider Ltd., Sustainalytics, Swaps Monitor, Tradeweb, United Nations, US Department of Commerce, Visible Alpha, Wells Bay, Wind Financial Information LLC, With Intelligence, Wood Mackenzie Limited, World Bureau of Metal Statistics, World Economic Forum, and YieldBook. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy. Data leveraged from third-party providers, related to financial and non-financial characteristics, may not be accurate or complete. The data and factors that Bridgewater considers within its research process may change over time.

This information is not directed at or intended for distribution to or use by any person or entity located in any jurisdiction where such distribution, publication, availability, or use would be contrary to applicable law or regulation, or which would subject Bridgewater to any registration or licensing requirements within such jurisdiction. No part of this material may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without the prior written consent of Bridgewater® Associates, LP.

The views expressed herein are solely those of Bridgewater as of the date of this report and are subject to change without notice. Bridgewater may have a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Those responsible for preparing this report receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.