At Bridgewater, we look for opportunities in over 200 markets across 45 economies. Each market is a distinct building block—combine them well, and you can build a portfolio that is well balanced to the ways the world might surprise us, without playing defense or sacrificing upside. Today, investors are mostly making use of one type of building block: the US equity market, and the handful of companies that dominate it. As strong a building block as this is, we see a wealth of opportunity in other economies and asset classes that investors—especially individuals—have hardly begun to tap. These investments are both attractive on their own and are great complements to what investors already hold. Below I’m sharing some of our recent research that walks through the opportunities we see today. I hope you find it useful.

Karen Karniol-Tambour

Co-Chief Investment Officer, Bridgewater Associates

The content of this newsletter includes an abridged excerpt from the Bridgewater Daily Observations.

A Wealth of Opportunity

As investors have reaped the benefits of the incredible run-up in US stocks, they’re left with more exposure to them than ever before. At the same time, when we scan across global markets, we see a wealth of opportunity for investors to complement these holdings with other assets. Besides being attractive on their own, these assets offer valuable downside protection, which is itself another kind of opportunity (e.g., giving you maneuvering room to buy dips).

For example:

- Foreign companies offer cheaper valuations, at the same time as the fundamentals are becoming more supportive in several important economies.

- Bonds (once 40% of a standard portfolio) came to play a smaller and smaller role in portfolios as yields hovered near zero throughout the 2010s. Now, they are once again offering much more competitive yields, allowing investors to gain downside protection while still earning meaningful returns.

- Gold is supported by secular tailwinds, from lingering inflation concerns, to worries about unsustainable government borrowing, to rising geopolitical tensions, that are just beginning to play out.

A bit of perspective on investors’ starting point today: coming out of the financial crisis, households held about half their financial investments in equities; today, it has risen to about 80%. The only time it’s ever approached this level before was at the height of the dot-com bubble. Almost all of that is in the US. For better or worse, households’ financial fates have become more and more tied to the S&P.

So far, that has been a fantastic bet, and we still see the US equity market as having many attractive qualities, particularly within the tech sector. At the same time, there’s plenty of room for investors to make their portfolios more resilient without going on the defensive, by adding exposure to other economies and assets that present attractive opportunities. Such moves position investors to prosper across a wide range of possible futures by putting some of their investments into assets that can do well in different economic environments, and across different economies facing different pressures.

Even incremental shifts can be quite impactful. Below, we take a closer look at some of the opportunities we see today.

Equities Outside the US

You’ll get no disagreement from us that the US is home to some of the world’s most exceptional companies, and that’s part of what has made the US equity market such a standout performer compared to global peers. However, when you look beyond the Magnificent 7 to the “S&P 493,” they’ve produced very similar earnings growth to companies abroad. And yet, so much money has flowed into the US that these “other 493” now trade at a substantial premium. This is why more and more companies have started to list in the US, knowing that they’ll trade at a higher valuation just by being listed here. The flip side of this, you might say, is that companies abroad are effectively on sale—you can buy a comparable stream of earnings for less. In the context of a US-oriented portfolio, allocating some capital to these companies also increases resilience to a potential slowdown emanating from the US.

Besides the more attractive valuations, the fundamentals are becoming stronger in important pockets of Europe and Asia, which are starting to see some of the drivers of past strong US performance. For example, Germany has lifted its self-imposed constraints on fiscal support in order to fund a transformational expansion in defense and infrastructure. Meanwhile, foreign investors had traditionally avoided Japan and Korea given concerns about insufficient focus on maximizing shareholder returns, but these markets have begun to see strong inflows in recent months thanks to aggressive pushes for stronger corporate governance and capital efficiency.

Government Bonds

It used to be that bonds played a core role as the “40” in a standard 60/40 allocation. But as yields ground down toward zero throughout the 2010s, that threatened their traditional role as a steady source of return that could also offer a cushion in a slowdown. Investors gradually shifted away from fixed income, and within their fixed income allocations, shifted away from the safety of government debt toward riskier credit markets that offered more yield but at the cost of downside protection. Now, conditions have fundamentally shifted, and the economy can sustain more normal bond yields, so bonds can once again play their pivotal role. Investors are responding, beginning to rebuild their bond allocations.

Bonds can be especially attractive to individual investors with a long-term focus, because the return for holding them all the way to maturity is known in advance, so you don’t have to worry about fluctuations in yields along the way. While high government debts and deficits are certainly a risk worth noting, the risk can be mitigated by holding bonds across different economies, as well as holding gold (discussed below). Overall, bonds have a valuable place in a portfolio that we see as underrecognized in most portfolios today.

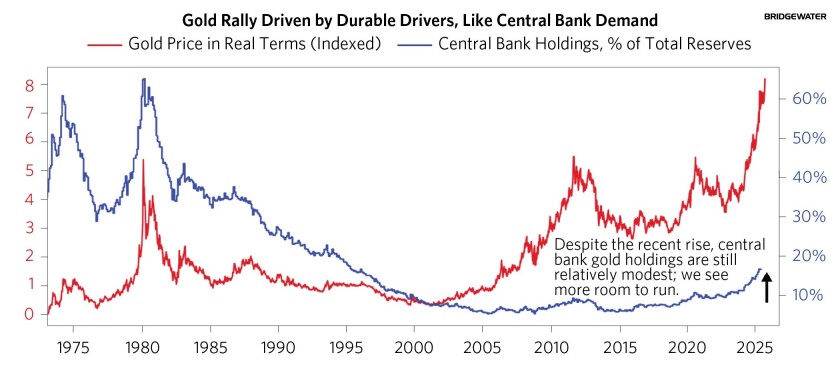

Gold

While gold has rallied materially, we still think it has value and provides downside protection for portfolios. It is notable that allocation shifts remain small, and secular pressures making gold more attractive seem unlikely to abate any time soon. Lingering inflation concerns, elevated public debts raising the prospect of future monetization, and rising geopolitical tensions have called the value of fiat money into question. Gold price action reflects a world where central banks and other investors are increasingly seeking to hedge monetary risk. In other words, there are large pools of capital that seem willing to buy gold at the current price and to accept the zero-yield opportunity cost of gold to buy down the risk of significant loss of capital from a geopolitical conflict or monetary debasement.

Putting It All Together

From foreign equity markets with cheap valuations and improving fundamentals, to bond markets that offer the opportunity to lock in yield and insulation from a slowdown, to a gold market whose rally thus far has been driven by forces that remain firmly in place, we see plenty of investments that are attractive on their own and can provide valuable downside protection. This offers investors the most important opportunity of all: creating a portfolio that is better balanced to different ways the world might play out, without playing defense or sacrificing upside.

This research paper is prepared by and is the property of Bridgewater Associates, LP and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, Bridgewater's actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing and transactions costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. Any such offering will be made pursuant to a definitive offering memorandum. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. No discussion with respect to specific companies should be considered a recommendation to purchase or sell any particular investment. The companies discussed should not be taken to represent holdings in any Bridgewater strategy. It should not be assumed that any of the companies discussed were or will be profitable, or that recommendations made in the future will be profitable.

The information provided herein is not intended to provide a sufficient basis on which to make an investment decision and investment decisions should not be based on illustrative information that has inherent limitations. Bridgewater makes no representation that any account will or is likely to achieve returns similar to those shown. The price and value of the investments referred to in this research and the income therefrom may fluctuate. Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur. Investments in hedge funds are complex, speculative and carry a high degree of risk, including the risk of a complete loss of an investor’s entire investment. Past performance is not a guide to future performance, future returns are not guaranteed, and a complete loss of original capital may occur. Certain transactions, including those involving leverage, futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Fluctuations in exchange rates could have material adverse effects on the value or price of, or income derived from, certain investments.

Bridgewater research utilizes data and information from public, private, and internal sources, including data from actual Bridgewater trades. Sources include BCA, Bloomberg Finance L.P., Bond Radar, Candeal, CBRE, Inc., CEIC Data Company Ltd., China Bull Research, Clarus Financial Technology, CLS Processing Solutions, Conference Board of Canada, Consensus Economics Inc., DataYes Inc, DTCC Data Repository, Ecoanalitica, Empirical Research Partners, Entis (Axioma Qontigo Simcorp), EPFR Global, Eurasia Group, Evercore ISI, FactSet Research Systems, Fastmarkets Global Limited, The Financial Times Limited, FINRA, GaveKal Research Ltd., Global Financial Data, GlobalSource Partners, Harvard Business Review, Haver Analytics, Inc., Institutional Shareholder Services (ISS), The Investment Funds Institute of Canada, ICE Derived Data (UK), Investment Company Institute, International Institute of Finance, JP Morgan, JSTA Advisors, LSEG Data and Analytics, MarketAxess, Medley Global Advisors (Energy Aspects Corp), Metals Focus Ltd, MSCI, Inc., National Bureau of Economic Research, Neudata, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Pitchbook, Rhodium Group, RP Data, Rubinson Research, Rystad Energy, S&P Global Market Intelligence, Scientific Infra/EDHEC, Sentix GmbH, Shanghai Metals Market, Shanghai Wind Information, Smart Insider Ltd., Sustainalytics, Swaps Monitor, Tradeweb, United Nations, US Department of Commerce, Verisk Maplecroft, Visible Alpha, Wells Bay, Wind Financial Information LLC, With Intelligence, Wood Mackenzie Limited, World Bureau of Metal Statistics, World Economic Forum, and YieldBook. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

This information is not directed at or intended for distribution to or use by any person or entity located in any jurisdiction where such distribution, publication, availability, or use would be contrary to applicable law or regulation, or which would subject Bridgewater to any registration or licensing requirements within such jurisdiction. No part of this material may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without the prior written consent of Bridgewater® Associates, LP.

The views expressed herein are solely those of Bridgewater as of the date of this report and are subject to change without notice. Bridgewater may have a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Those responsible for preparing this report receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.