The economy is now only moderately out of balance, with lagged effects from prior tightening likely ahead. What is more out of balance is the pricing of markets in relation to these conditions.

In recent months, markets have gradually recognized the unresolved dilemma that the Fed and other central banks face. Despite improvement, economies remain out of equilibrium, and the path to balance is likely to take a while. The result is generally characterized as short-term interest rates staying “higher for longer.”

This “higher for longer” situation will persist until key conditions coalesce near their sustainable equilibriums. Most or all of the components must come together because they interact with one another to bring about sustainable outcomes. As we see it, an economy is in a sustainable equilibrium to the extent that all three of the following conditions are broadly in place:

- Spending is in line with output.

- Debts are in line with incomes.

- The risk premiums on assets relative to cash and to one another are roughly in line with their relative risks.

We see the mechanics of these conditions working as follows:

When spending is in line with output you can have sustainable positive economic growth with sustainable low inflation. More specifically, this occurs when nominal spending growth is in line with the growth in the labor force and productivity (e.g., nominal growth around 4% in the US), and the levels of output and employment are about right in relation to the level of output capacity and the size of the labor force.

When debts are in line with income you have neither the vulnerability of a debt bubble that can be popped by a tightening of monetary policy (e.g., the 2008 financial crisis), nor a spiraling credit contraction that sends the economy into a self-reinforcing deflationary depression (e.g., the Great Depression). This balance also applies to the major sectors of an economy because the parts of an economy interact with one another. A smoothly functioning economy requires them to work together in self-reinforcing unison.

When risk premiums are in line with their risks this supports the free flow of capital to support the economy. For example, a moderately upward-sloping yield curve encourages a sustainable degree of risk-taking to generate credit growth. And a reasonable risk premium in equities relative to bonds encourages a sustainable flow of equity capital into productive enterprise and a lower chance of destabilizing price movements.

The short-term interest rate is a key variable in managing these conditions and is once again the central bank’s primary policy lever (since interest rates are far enough above zero). The central bank pulls the lever in order to steer the economy toward equilibrium. This is challenging when you start from a major disequilibrium because policy actions affect changes in spending, output, and inflation with significant lags (the process can take years), and in the meantime markets are responding to central bank actions and having their own impact on the path of the economy. So, a lot of judgment and guesswork is required. “Data-dependent” decision making is an over-simplification because data about the future does not yet exist.

Currently in the US, economic conditions and interest rate pricing have moved toward equilibrium over the last few months but are not there yet. Since the level of growth is about average while labor markets are strong, the economy is not currently calling for a cut in interest rates, and at the same time the level of inflation is still higher than desired. A rise in interest rates is now happening on the long end, drawn higher by the need for an acceptable risk premium relative to the current level of T-bill rates in order to clear high levels of supply. This is likely to be sustained until conditions call for a change. And equity market pricing looks further out of equilibrium, as valuations remain high even with substantially higher long-term interest rates.

This struggle to achieve a balance of conditions has been going on for four years now and probably has a couple of years left to run given the normal linkages (assuming good policy decisions and no more shock events). In 2019, economies were near equilibrium after a decade of deleveraging and balance sheet restructuring from the prior excesses. Then the pandemic caused a big down, followed by a big reflation, which caused an overshoot, then tightening, which produced a big down, leading to where we are now. Taking stock of where we are now, the above conditions have not been met. There has been steady progress, including the rise in bond yields and the decline in stock prices over the past three months, which have felt bad, but are actually movements toward equilibrium.

To illustrate current conditions, the path that we’re on, and the interaction of the parts, we will walk through a few high-level charts. We’ve scaled them all to common terms, so that the degree of imbalance in one condition can be seen in relation to the others. Here we are only showing the US, but each economy has its own story. Europe and the UK have a lot in common with the US. China is out of balance on the downside (weak growth, low inflation). And Japan is in the ballpark of a sustainable equilibrium.

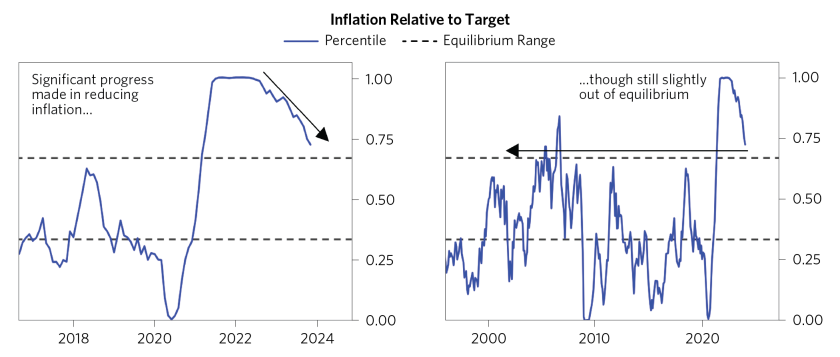

We start with the level of inflation, which is the primary imbalance. Inflation has fallen but remains materially above the target. It is moving in the right direction and approaching the upper end of an acceptable range but is not there yet—and shows signs of leveling out given the persistence of higher-than-equilibrium wage growth. The chart on the left zooms in to recent trends, and the chart on the right puts current conditions in the context of a longer history.

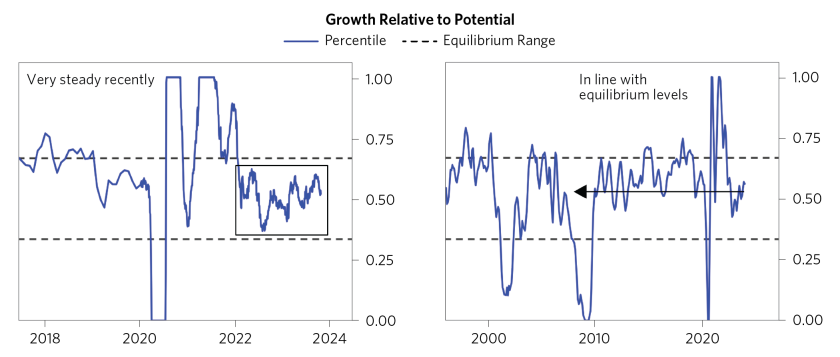

Real growth remains around target. Below, we show our coincident read on the underlying rate of real growth, which is less sensitive to the volatility in quarterly GDP reporting. Leading measures suggest weakness ahead, but given the resilience of the economy to tightening so far, that won’t carry much weight in the policy-making decision process today.

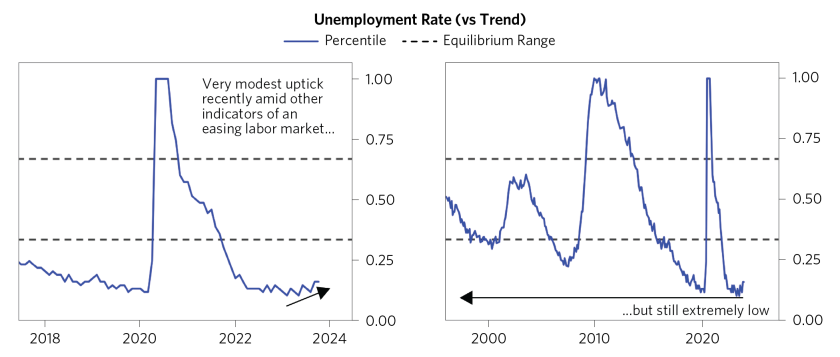

At this time when inflation is higher than desired and growth is about right, the level of unemployment remains low. The combination of low unemployment and positive growth is creating a supply/demand condition for labor, which is slowing the rate at which wages and inflation can fall. That said, unemployment has ticked up a bit in recent months, due mainly to an increase in labor market participation, amid broader signs of easing in the labor market—in particular, job openings falling and wage growth easing slightly. All of this represents small moves toward equilibrium.

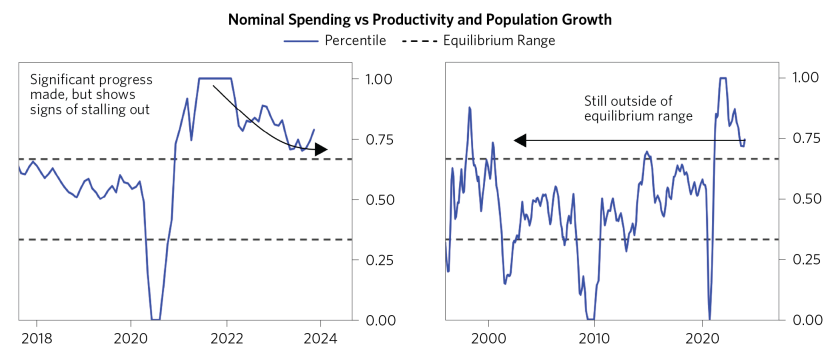

Nominal spending is way down from highs in response to the tightening—down from 10% nominal growth a year ago—but the current level of nominal spending growth remains too high, and the most recent GDP reporting (consistent with timely stats) shows a recent leg up.

Netting the balance of current economic conditions, nominal spending is too high relative to output, output is too high relative to capacity, inflation is higher than desired, and real growth is about right. The economy is now only moderately out of balance, with lagged effects from prior tightening likely ahead. The right policy response to these conditions is to hold short-term interest rates roughly where they are, or possibly raise them a bit more if the economy doesn’t weaken—i.e., “higher for longer” than what markets have been discounting.

What Is More Out of Balance Is the Pricing of Markets in Relation to These Conditions

Bond yields remain well below cash rates at a time when there is really no pressure to lower short-term interest rates given current conditions. This inversion of the yield curve has been helped along by the combination of the Fed raising short-term interest rates while liquidity has remained plentiful on the long end of the yield curve due to the Treasury funding the deficit with T-bills, which in turn were financed by a substantial residual of excess liquidity from prior QE.

Again, the recent rise in bond yields has been a move toward equilibrium, helped along by increased supply on the long end of the yield curve. And if conditions weaken and short-term rates ease in line with what is priced in, long-duration yields look much more attractively priced.

Within the interest rate structure, there is now a fairly attractive risk premium on inflation-indexed bonds (i.e., the real yield) relative to the market’s discounting of the future real yield of cash (the discount rate). This reflects that long-term inflation expectations remain anchored at the Fed’s target such that rising nominal rates have resulted in reasonably high levels of real yields and an upward-sloping real yield curve, relative to discounted future real short-term interest rates. Again, the recent rise in real yields has been a move toward equilibrium.

The above risk premium calculation is based on long-term real yields relative to the market’s discounting of real short-term interest rates a few years from now, which are priced to decline from current levels. Current imbalances, as described above, are inconsistent with such a decline, and easing in line with what’s discounted would require more material economic weakness. Again, the recent rise in forward cash yields has been a movement toward equilibrium.

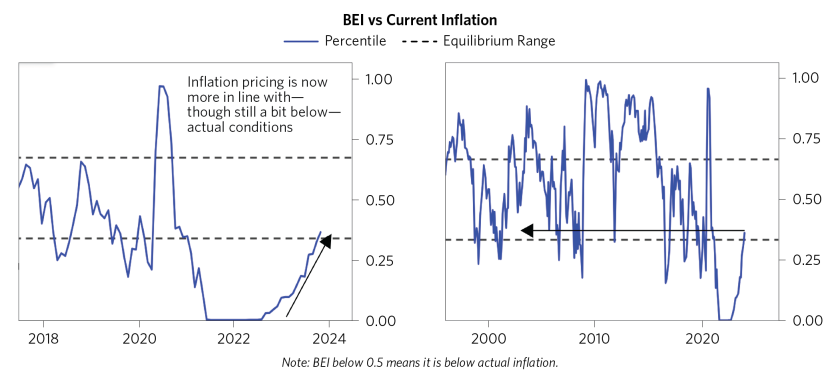

Markets continue to discount a future level of inflation near target, which is below current inflation rates. This is not unreasonable because the Fed does have the ability to finish the job and, at some point in the future, to bring the inflation rate to the target, even if it takes a while to achieve that along with the other requirements for a sustainable equilibrium. The main risk to breakevens is a change in the Fed’s willingness to do whatever it takes to achieve the goal (i.e., a willingness to tolerate sustained above-target inflation in the context of other economic conditions), a risk that would be most acute at the time of a turnover in the Fed chair (Powell’s term is up in 2026).

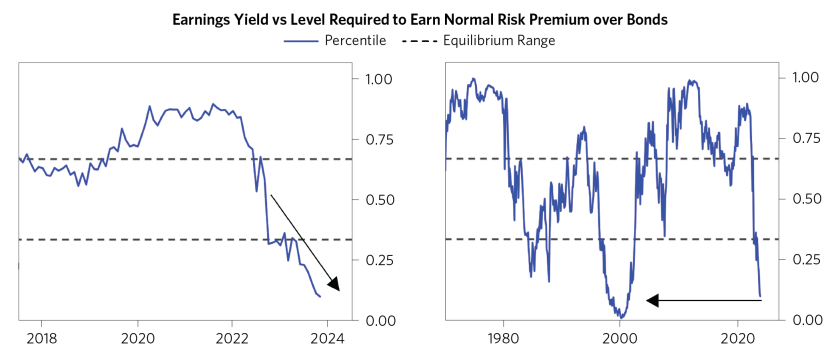

Since this tightening cycle began, there has been a persistent outperformance of equities relative to bonds, which has compressed the risk premium on equities relative to bonds. Like the yield curve inversion, this contraction in risk premiums was supported by the residual excess liquidity produced by QE, and the lack of long-duration Treasury supply freeing up that liquidity to flow into the equity market. Below, we show an estimate of the current equity forward earnings yield, relative to the level required to earn a normal risk premium over bonds if earnings grow in line with the overall economy. Recently, equity yields have changed little as bond yields have risen significantly, such that equity pricing has moved further from equilibrium. The last time we were here was 2000, which was followed by a decade of poor equity returns.

This research paper is prepared by and is the property of Bridgewater Associates, LP and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, Bridgewater's actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing and transactions costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. Any such offering will be made pursuant to a definitive offering memorandum. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice.

The information provided herein is not intended to provide a sufficient basis on which to make an investment decision and investment decisions should not be based on simulated, hypothetical, or illustrative information that have inherent limitations. Unlike an actual performance record simulated or hypothetical results do not represent actual trading or the actual costs of management and may have under or overcompensated for the impact of certain market risk factors. Bridgewater makes no representation that any account will or is likely to achieve returns similar to those shown. The price and value of the investments referred to in this research and the income therefrom may fluctuate. Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur. Investments in hedge funds are complex, speculative and carry a high degree of risk, including the risk of a complete loss of an investor’s entire investment. Past performance is not a guide to future performance, future returns are not guaranteed, and a complete loss of original capital may occur. Certain transactions, including those involving leverage, futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Fluctuations in exchange rates could have material adverse effects on the value or price of, or income derived from, certain investments.

Bridgewater research utilizes data and information from public, private, and internal sources, including data from actual Bridgewater trades. Sources include BCA, Bloomberg Finance L.P., Bond Radar, Candeal, Calderwood, CBRE, Inc., CEIC Data Company Ltd., Clarus Financial Technology, Conference Board of Canada, Consensus Economics Inc., Corelogic, Inc., Cornerstone Macro, Dealogic, DTCC Data Repository, Ecoanalitica, Empirical Research Partners, Entis (Axioma Qontigo), EPFR Global, ESG Book, Eurasia Group, Evercore ISI, FactSet Research Systems, The Financial Times Limited, FINRA, GaveKal Research Ltd., Global Financial Data, Inc., Harvard Business Review, Haver Analytics, Inc., Institutional Shareholder Services (ISS), The Investment Funds Institute of Canada, ICE Data, ICE Derived Data (UK), Investment Company Institute, International Institute of Finance, JP Morgan, JSTA Advisors, MarketAxess, Medley Global Advisors, Metals Focus Ltd, Moody’s ESG Solutions, MSCI, Inc., National Bureau of Economic Research, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Refinitiv, Rhodium Group, RP Data, Rubinson Research, Rystad Energy, S&P Global Market Intelligence, Sentix Gmbh, Shanghai Wind Information, Sustainalytics, Swaps Monitor, Totem Macro, Tradeweb, United Nations, US Department of Commerce, Verisk Maplecroft, Visible Alpha, Wells Bay, Wind Financial Information LLC, Wood Mackenzie Limited, World Bureau of Metal Statistics, World Economic Forum, YieldBook. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

This information is not directed at or intended for distribution to or use by any person or entity located in any jurisdiction where such distribution, publication, availability, or use would be contrary to applicable law or regulation, or which would subject Bridgewater to any registration or licensing requirements within such jurisdiction. No part of this material may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without the prior written consent of Bridgewater® Associates, LP.

The views expressed herein are solely those of Bridgewater as of the date of this report and are subject to change without notice. Bridgewater may have a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Those responsible for preparing this report receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.